By Frances A. Tomes, Esq. Tax Attorney, Helping Small business and individuals for over 30 years

Quick Answer: A bank levy or wage levy by the IRS or State of New Jersey causes consequences and stress but you may still have options to stop or release the levy. Depending on your circumstances, solutions may include an Installment Agreement, Currently Not Collectible status, an Offer in Compromise, or proving financial hardship. The most important thing you can do is act quickly.

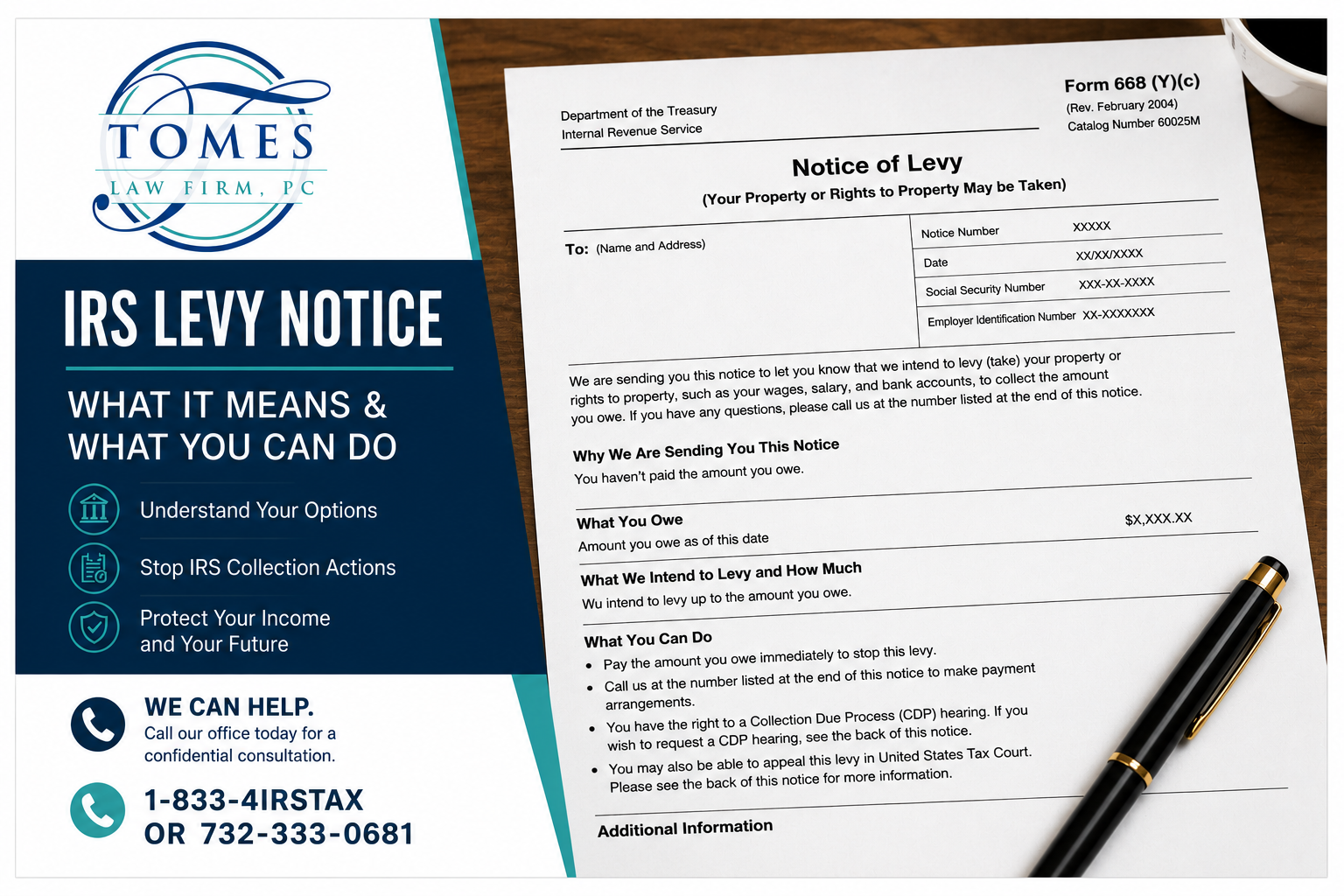

Can the IRS Levy My Bank Account for Back Taxes?

Yes.

If you owe back taxes and have not resolved the debt, the IRS can levy your bank account and seize funds to satisfy the tax liability.

Many taxpayers are surprised to learn that an IRS bank levy does not happen overnight. Before issuing a levy, the IRS generally sends multiple notices and provides opportunities to resolve the debt.

Once the bank receives the levy, the funds in your account are typically frozen. However, there is often a limited window of time before the money is sent to the IRS, which may allow you to pursue options to have the levy released.

The key is acting quickly.

What Should I Do If the IRS Levied My Bank Account?

If the IRS has levied your bank account:

- Do not ignore the levy notice.

- Determine how much tax debt you owe.

- Review all IRS notices you have received.

- Contact a qualified tax resolution attorney immediately.

- Explore available collection alternatives before the funds are transferred.

Many people panic and assume the money is gone forever. In some cases, there may still be opportunities to stop or release the levy, depending on your circumstances.

Can the IRS Garnish My Paycheck?

Yes.

An IRS wage levy allows the government to take a portion of your paycheck until the tax debt is resolved or the levy is released.

Unlike many other creditors, the IRS does not need a court judgment before garnishing wages for unpaid federal taxes.

For many taxpayers, a wage levy creates immediate financial hardship, making it difficult to pay rent, mortgages, utilities, and other necessary living expenses.

Why Did This Happen?

Most people who owe back taxes are not trying to avoid paying.

Life happens.

I’ve worked with clients who fell behind because of:

- Job loss

- Divorce

- Medical issues

- Business setbacks

- Unexpected tax bills

- Economic hardship

The IRS generally does not stop collection efforts simply because someone is struggling financially. If tax debt remains unresolved long enough, collection action often follows.

That doesn’t mean you’re out of options.

How Can I Stop an IRS Levy?

The IRS may release a levy when:

- You enter into an approved payment arrangement.

- The levy is creating economic hardship.

- The tax debt is resolved.

- The levy was issued improperly.

- Another collection alternative is accepted.

The right solution depends on your unique financial situation.

Some taxpayers qualify for an IRS Installment Agreement, which allows them to make affordable monthly payments over time.

Others may qualify for Currently Not Collectible Status, which can temporarily stop IRS collection activity when paying the tax debt would prevent them from meeting basic living expenses.

In some situations, taxpayers may even qualify for an Offer in Compromise, which allows them to settle their tax debt for less than the full amount owed.

Every case is different, which is why a thorough review of your finances and IRS records is critical.

What Happens If I Ignore an IRS Levy?

Ignoring an IRS levy can lead to:

- Continued wage garnishments

- Additional bank levies

- Seizure of future tax refunds

- Collection actions against business assets

- Increased penalties and interest

- Greater financial stress

One of the biggest mistakes I see is people doing nothing because they feel overwhelmed. I understand that feeling. Tax problems create anxiety. Many people avoid opening IRS letters because they are afraid of what they might find. Unfortunately, waiting often reduces the number of available solutions.

Frequently Asked Questions

Can an IRS levy be removed?

Yes. In many situations, a levy can be released if you qualify for a collection alternative, demonstrate financial hardship, or resolve the underlying tax debt.

How long does an IRS bank levy last?

A bank levy generally affects the funds in the account at the time the levy is received. Timing is critical because there is often a limited opportunity to intervene before the funds are transferred to the IRS.

Can the IRS take all the money in my bank account?

The IRS can seize funds up to the amount of the tax debt, subject to applicable procedures and limitations.

What is the best way to stop an IRS levy?

The best solution depends on your financial circumstances. Common options include an Installment Agreement, Currently Not Collectible status, proving economic hardship, or resolving the debt through an Offer in Compromise.

Can an attorney help remove an IRS levy?

Yes. A tax resolution attorney can review your IRS account, determine whether the levy can be challenged or released, negotiate directly with the IRS, and identify the most effective resolution strategy.

Can the IRS freeze a joint bank account?

Yes. If your name is on a joint bank account, the IRS may levy funds in the account even if another person contributed some or all of the money. If a joint account holder believes the levied funds belong to them, they may have options to challenge the levy.

How long does it take the IRS to release a levy?

The timing varies depending on the circumstances. In some cases, the IRS may release a levy relatively quickly after approving a payment arrangement or determining that the levy is causing economic hardship. The sooner you address the issue, the sooner a release may be possible.

Can the IRS levy Social Security benefits?

Yes. The IRS may levy a portion of certain federal payments, including Social Security benefits, through programs designed to collect unpaid tax debt.

Can the IRS levy a business bank account?

Yes. If a business owes unpaid taxes, the IRS may levy business bank accounts and other business assets. This can create serious cash flow problems and make it difficult to operate the business. Business owners should act quickly to explore available resolution options.

What is the difference between an IRS lien and an IRS levy?

An IRS lien is a legal claim against your property because of unpaid taxes. An IRS levy is the actual seizure of money or property to satisfy the tax debt. In simple terms, a lien is a claim, while a levy is the action of taking assets.

Can the IRS take money from my bank account without warning?

Generally, the IRS must send notices and provide an opportunity to resolve the debt before issuing a levy. Many taxpayers are surprised by a levy because they did not realize the earlier notices required immediate attention.

Can the IRS levy my paycheck and bank account at the same time?

Yes. In some situations, the IRS may pursue multiple collection actions simultaneously. This is one reason it is important to address tax debt before collection activity escalates. Unlike most creditors, the IRS is not limited to 10% of your paycheck on a wage garnishment.

Will filing bankruptcy stop an IRS levy?

In some cases, bankruptcy may stop IRS collection activity through the automatic stay. However, not all tax debts are dischargeable, and the interaction between bankruptcy law and tax law can be complex. An experienced attorney can evaluate whether bankruptcy may be an option in your situation. Here at Tomes Law Firm we have been helping New Jersey people with tax debt and bankruptcy for decades

What if I cannot afford to pay my tax debt?

If paying the tax debt would prevent you from meeting necessary living expenses, you may qualify for relief programs such as an Installment Agreement, Currently Not Collectible status, or an Offer in Compromise. The best option depends on your financial circumstances.

What tax relief programs are available if I owe back taxes?

Potential tax relief options include:

- Offer in Compromise

- Installment Agreements

- Currently Not Collectible Status

- Penalty Abatement

- Innocent Spouse Relief

- Other IRS collection alternatives

The right option depends on your income, assets, expenses, and overall financial situation.

You May Have More Options Than You Think

Many taxpayers believe their only option is to pay the IRS in full. Fortunately, that is often not the case.

Depending on your circumstances, you may qualify for an Offer in Compromise, a monthly Installment Agreement, Currently Not Collectible Status, penalty relief, or other tax resolution programs designed to help taxpayers get back on track.

I’ve helped many individuals and small business owners who thought they had no way out of their tax problems. In many cases, there were solutions available that they simply didn’t know existed.

Receiving an IRS levy notice is frightening, but it does not necessarily mean you’re out of options.

Final Thoughts

If you’re searching for answers about IRS bank levies, wage garnishments, back taxes, tax debt relief, Offer in Compromise programs, or how to stop IRS collections, you’re not alone. Every year, New Jersey taxpayers contact our office after receiving an IRS levy notice, believing there is nothing they can do. In many cases, options are still available—but timing is critical. In reality, many taxpayers qualify for solutions that can stop collection activity and help them regain control of their finances. The key is acting before the situation becomes more difficult—and more expensive—to resolve.

If the IRS has levied your bank account, garnished your wages, or is threatening collection action, don’t wait to find out what options may be available. The sooner you take action, the more opportunities you may have to protect your income, resolve your tax debt, and move forward with confidence.

At Tomes Law Firm, we focus on helping individuals and small business owners resolve IRS tax problems, including bank levies, wage garnishments, tax liens, and unfiled tax returns. Attorney Frances Tomes has helped taxpayers navigate complex IRS collection matters and pursue solutions that fit their financial circumstances.

Tomes Law Firm is based right here in New Jersey and works exclusively with New Jersey individuals and small business owners. When you call us, you’re talking to someone local — someone who understands the specific challenges of running a business in this state.

Call us today: